This week’s video transcript summary is here. You can click on any bulleted section to see the actual transcript. Thanks to Granola for its software.

Editorial

What Time is it?

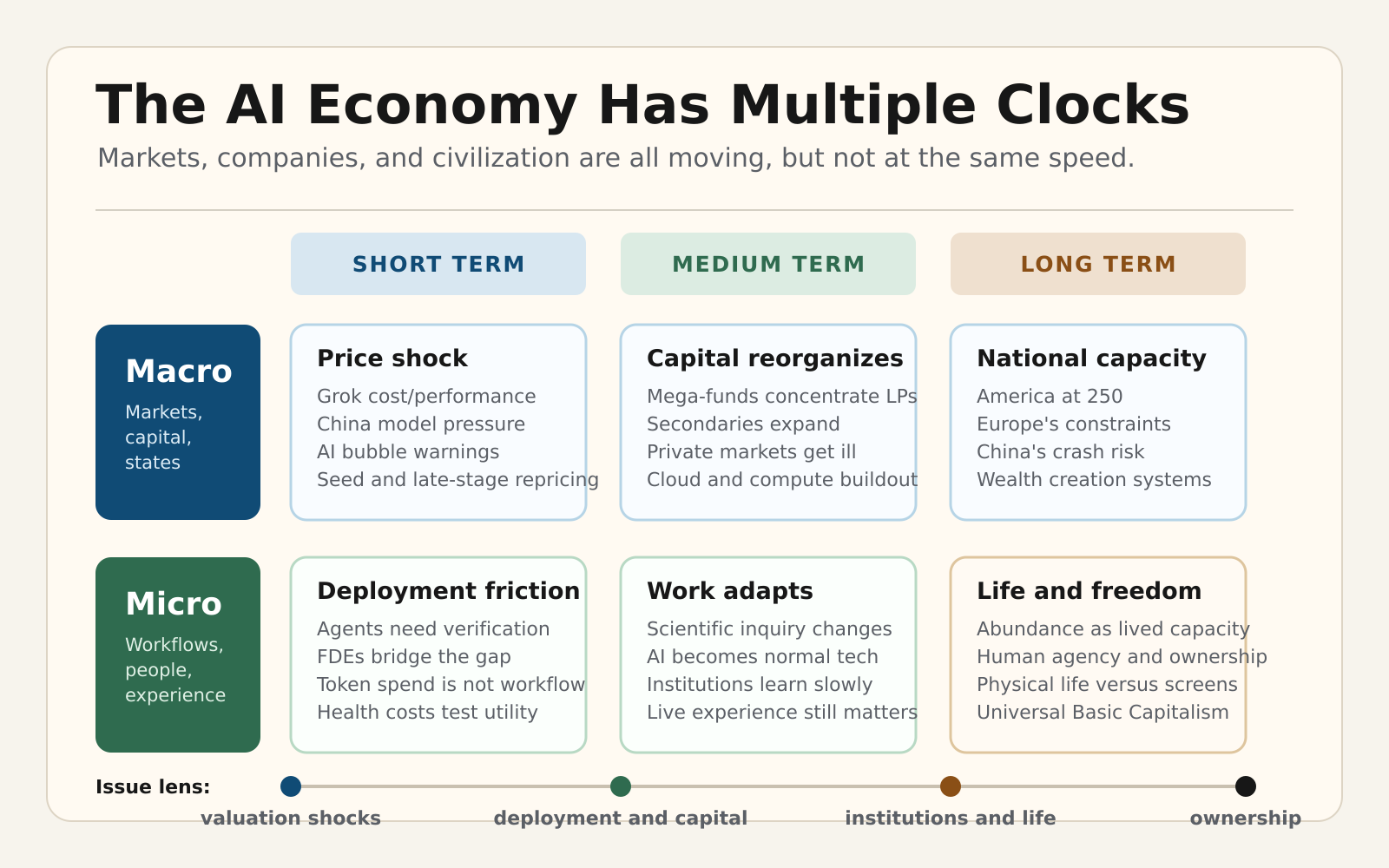

The AI Economy Has Multiple Clocks

Grok 4.5 arrived this week with a simple promise: near-frontier intelligence, faster and cheaper. A lot cheaper.

Elon Musk called it “Opus-class, but faster, more token-efficient and lower cost.” xAI called it its “first model trained specifically for coding and agents.”

That is a product launch. It is also a price signal. And OpenAI launched ChatGPT 5.6 as a far more efficient user of tokens than Anthropic. Costs again. Everybody is talking about the price of tokens.

This week I kept trying to find one theme and kept finding several. That is usually a sign that the theme is hiding one level higher.

AI is not one story. It is a market story, a deployment story, a capital and infrastructure story, and a civilization story. And they are all on different timelines. The mistake is to force all of those clocks to show the same time.

The first clock is short term - price

The short term clock is governed by price. The Grok 4.5 argument is not only whether it is smart. It is whether it is smart enough at a price that changes buyer behavior. Latent.Space’s coverage puts the launch on the cost/performance frontier, not merely the benchmark frontier.

That matters because price is the first way a technology becomes economic. A thing can be brilliant and irrelevant if it is too expensive to use often. A thing can be slightly less brilliant and transformative if it is cheap enough to be everywhere.

The same price clock shows up in China. CNBC reports that Chinese models have accounted for more than 30% of tokens used by U.S. companies every week since February 8, peaking at 46%. That is not driven by ideology. That is logic and math driving procurement.

If a model is 60% to 90% cheaper and good enough for a large class of tasks, engineers will route work to it. They should. In the short term, the market is discovering that “frontier” and “useful” are related but not identical categories.

The venture version of the price clock is valuation. Terrence Rohan calls the current top 5% of seed deals “the worst asset class in venture” and summarizes the trade as “Seed risk at Series B prices.” Risk has not moved down as fast as price has moved up. Seed companies are still seed companies. They can still fail like seed companies. But the top of the market is starting to price some of them as if the future has already happened.

So yes, there is froth. Treasury analysts are apparently worried enough to model an AI pullback as a financial-stability issue. Samir Kaji is right that venture is living through a genuine AI supercycle and an obvious late-cycle bubble at the same time. Both can be true. Most AI companies can be overvalued and a few can still become the largest companies ever created.

That is the first clock. Markets are repricing AI in real time.

The second clock is also a short term one - deployment.

This is where the AI story gets less glamorous and more important. Aaron Levie says enterprise IT leaders are moving away from token counts as the main adoption metric and toward business outcomes. That is inevitable. Nobody should care how many tokens a company consumes if the workflow stays the same, the customer experience stays the same, and the P&L does not move. So what to deploy is the form taken by market penetration. Anthropic is a net loser in this equation.

The hard part is that enterprises do not run as neat prompts. They run through silos, legacy systems, messy permissions, fragmented data, and people who are accountable when something breaks. Levie’s point is that agents are most useful when they cross those boundaries. That means the problem is no longer just model capability. It is ownership, adoption, data access, measurement, and responsibility.

OpenAI’s ChatGPT Work announcement makes that shift explicit. The pitch is no longer a smarter chatbot. It is an agent that can gather information across apps, create sheets, slides, docs, and web apps, and stay with complex projects for hours. OpenAI says more than 5 million people use Codex every week and more than 1 million now use it outside software development. That is the tell. Coding agents are becoming work agents. And the consolidation of Codex and Chat into a single new app (with an old name - ChatGPT) that includes ‘Work’ shows OpenAI means business (pun intended).

Nate’s piece on agent trust says the same thing from a different direction. The answer is not waiting for a model that never hallucinates. The answer is verifying the work, not worshipping the model. His $8 multi-agent website run is funny because it is so familiar: one agent fabricated thirteen quotes and certified the work as flawless. The system only worked because other agents caught the failures, documented them, forced rework, and verified the output. This is a loop, and if you are not using it, you should be.

Real institutions adopt new capabilities, not simply by believing, they inspect.

The Bun rewrite is the same lesson in production engineering. Jarred Sumner says Bun was moved from Zig to Rust after years of stability work still left the project exposed to memory leaks, use-after-free crashes, double frees, and other failures. The remarkable part is not just that AI agents helped port more than 500,000 lines of code in 11 days. It is that the process required adversarial reviewers, workflow rules, compiler feedback, test suites, fuzzing, and human supervision. The productivity story and the verification story are the same story.

Education is the same problem with higher stakes. Jessica Blake’s Brown story in ‘Inside Higher Ed’ is not really resolved by better policing.

Roberto Serrano suspects much of his welfare economics class used AI on a take-home midterm, saw the average jump to 96 percent, then moved the final back in person and watched the average fall to 48.6 percent. Brown’s own GenAI report says “There is no way to check with 100 percent accuracy whether GenAI has been employed” and urges faculty to “de-emphasize punishment.”

Serrano ends with the opposite fear: “We cannot choose to become idiots.” Both are right. Students will use AI. My opinion is that the institution’s job is to reward good use, punish fake work, and test intelligence, familiarity with process, and familiarity with content. Using AI does not have to be cheating. But of course it can also be cheating. There is no future higher ed without AI, that is a pipe dream.

Teaching use of AI is why the forward-deployed engineering boom matters. Tomasz Tunguz says AI companies have committed $9.75 billion in 12 months to FDE teams because the bottleneck has shifted from model capability to enterprise deployment.

That is a staggering number, but it makes sense. Powerful models do not automatically know how a hospital, a bank, a manufacturer, or a media company actually works. Somebody has to sit with the customer long enough to translate capability into operating change.

Health care shows the trap. Bob Kocher, Brian Zhao, and Erin Duffy argue that AI may raise U.S. health care spending in the short to medium term unless payment models change.

Better tools can produce more visits, tests, prescriptions, referrals, drug discovery, monitoring, and administrative activity. In a bad incentive system, productivity can become more billable volume rather than lower cost. AI does not automatically fix institutions. It amplifies the rules it enters.

That is the deployment clock. Companies, schools, and health systems are learning how to use AI. Not demo it. Use it.

The third clock is medium term - capital and infrastructure.

Pavel Prata’s mega-fund chart is a useful warning. Fourteen funds represented only 6.7% of fund count but controlled 65% of all capital raised in the first half of 2026. Andreessen Horowitz alone raised $15 billion, more than the bottom 168 funds combined. Thrive added $10 billion. Two firms collected roughly one third of H1 2026 capital.

That is not a normal venture market. It is a capital-allocation machine being rebuilt around AI, defense, space, compute, and private-company duration.

Turner Novak’s secondaries post adds the liquidity side. VC secondaries have grown “from a $250M to $150B market over the past 25 years,” and one of the questions in that market is “what happens after SpaceX, OpenAI, Anthropic IPOs.” That is not a side question. It is the question of how private markets absorb companies that take longer to mature, require more capital, and create wealth before the public ever gets access.

Dan Gray calls venture the sick man of private markets because the fund model is showing strain. His proposed answer is not a retreat from ambition. It is a more serious financing model for reindustrialization: small funds to discover, venture philanthropy to support early strategic technologies, and giant pools of capital to fund deployment. That is probably closer to what the AI buildout needs than the old story of two engineers, a laptop, and a Series A.

Infrastructure says the same thing. M.G. Siegler’s “Elon Lever” is the observation that SpaceX and xAI turned surplus compute from a cost problem into a cloud revenue narrative. Chris Zeoli points out that networking is already 10% to 15% of cluster cost and that frontier runs often sustain under 50% utilization. Rebecca Kaden writes about data at the edge, where AI moves the software flywheel into the body, the ocean, robotics, infrastructure, weather, and ambient conversation.

In other words, AI is not becoming less physical as it gets more intelligent. It is becoming more physical. More data centers. More power. More networks. More robots. More sensors. More edge devices. More capital.

This is why the short-term bubble conversation can be true and still not be enough. Bubbles are about price. Buildouts are about capacity. The hard part is that both happen at the same time.

The fourth clock is long term - civilization.

Arvind Narayanan calls AI a “normal technology.” I like that phrase because it deflates hysteria without deflating importance. Electricity was a normal technology. The internet was a normal technology. Normal technologies do not change the world by magic. They enter institutions, change workflows, create new jobs, destroy old ones, and take longer than their loudest advocates expect.

Narayanan’s “decide, execute, deliver sandwich” is a useful framework. AI may compress the execution layer, but humans still decide what is worth doing, verify quality, integrate the result, and accept responsibility. That does not make AI small. It makes it adoptable. It also means the labor question is not simply “will AI replace jobs?” The better question is: which parts of work become cheaper, which parts become more valuable, and who owns the system of record when the change is finished?

John Battelle’s essay pushes this into life itself. He quotes Ian Bogost’s line that “our lives have become dematerialized” and asks whether software has eaten the world without anyone asking what the meal costs. That is not anti-technology. It is a humanist question. If every layer of experience is mediated through “smoothed glass and pixels,” then abundance cannot just mean more computation. It has to mean better life. Actually more computation may be the only way to get to a better life.

The Eventbrite story belongs here too. The internet did not replace real-life gathering. It made discovery easier, ticketing easier, payments easier, promotion easier. But the thing people wanted was still physical presence. That is an important corrective to the pure digital story. Humans still want to be in rooms together. Less time spent earning a wage will facilitate that.

Noah Smith asks whether America’s 250th anniversary is really about the end of “the human age.” Ivan Krastev asks why America has lost faith in itself. Krugman complicates the lazy Europe-versus-America story by noting that Europe still offers more leisure, lower inequality, and longer life expectancy even if it has missed the AI boom.

Matthew Yglesias brings it home through housing. Capitalism is hard to defend to young people when the thing they need most is made scarce by law. If private ownership exists inside a system where building is blocked, delayed, and rationed, people experience the result as failure. They are not wrong to notice.

This is where last week’s theme - Universal Basic Capitalism - fits. Andrew Keen framed the question as whether citizens should become shareholders in AI-created wealth rather than recipients of welfare managed by a larger state. That was his summary of last week’s show.

He quotes my line from the interview: “The pinnacle of capitalism is still flawed. Any idea that it’s perfect - this idea of the perfect union - is deeply flawed as a concept and always has been.”

That is the point. The answer to capitalism’s flaws is not to pretend they do not exist. Nor is it to abandon the wealth-creation machine just as it is about to become more powerful. The answer is to make ownership broader, make deployment real, make institutions faster, and make the benefits visible in ordinary life.

Sam Altman’s proposed 5% public stake in OpenAI belongs in this argument, whether one likes the mechanism or not. The Wall Street Journal frames it as “more regulation, more taxation and even partial government ownership.” Maybe that is right. Maybe it is too clever by half. But the instinct behind the debate is real: if AI creates extraordinary wealth and dislocates work, the ownership question cannot be left until after the fact.

There are political risks in having civilizational opinions. The Wall Street Journal’s other OpenAI and Anthropic piece makes the useful distinction. Anthropic’s fight with Washington is acute: access, procurement, military use, and national-security suspicion. OpenAI’s exposure is more structural because it is becoming a consumer platform, enterprise vendor, national infrastructure candidate, and geopolitical asset at the same time. Companies that become that important do not get to remain merely companies. They become political objects.

That is why the ownership question matters. If AI companies are going to be treated as infrastructure, if their models shape work and education, if their compute becomes a national asset, and if their wealth creation is large enough to change the distribution of opportunity, then the social contract cannot be an afterthought. The point is not to nationalize intelligence. The point is to make sure the wealth-creation machine produces citizens with more agency, not only institutions with more power.

So the issue is not whether AI is a bubble or a revolution. It is both, on different clocks.

In the first clock, prices and valuations are moving faster than certainty. In the second, deployment is colliding with institutions. In the third, capital and infrastructure are reorganizing around the buildout. In the fourth, the question is whether all of this produces better lives, more freedom, and a civilization that knows what to do with abundance.

That last word still matters. Abundance is not just GDP. It is not just model capability. It is not just cheaper tokens. Abundance is economic success plus life experience plus personal freedom. It is the capacity to build, to own, to move, to gather, to work, to learn, and to live better.

The AI economy has multiple clocks. The mistake is reading only one of them.

Post of the Week notes the passing of David Potter. I first met David in 1996 when EasyNet was about to be listed on the AIM market in London. We were seeking investment from his very successful company - Psion. We didn’t get it :-)

David was an entrepreneur and innovator. He was deep in science, very opinionated, and intensely aware of opportunity. In later life, due to family connections, I got to know him quite well. He will be missed, but his impact on the history of technology is permanent.

Contents

Essays

AI

Treasury Has an Internal Report Warning About the Dangers of an AI Bubble

Chinese AI models are gaining ground with U.S. companies as OpenAI, Anthropic costs surge

AI agents move deeper into business workflows with ChatGPT Work & GPT-5.6

Thinking about the Impact of Artificial Intelligence on U.S. Health Care Costs and Spending Growth

Venture Capital

Regulation

Infrastructure

Interview of the Week

Startup of the Week

Post of the Week

Essays

The American age was the human age

Noah Smith uses America’s 250th anniversary to ask whether the country’s problem is collapse, sclerosis, or something larger: the end of a human-centered age. He argues that the United States is not in an obvious terminal phase. GDP remains on its long upward trend, the economy is still robust, AI is “upending the world,” and everyday consumer convenience keeps working even as health care, transit, cities, and politics feel broken.

The essay’s central concern is that the country has grown comfortable with stasis. Smith points to local veto power that blocks or delays factories, housing, energy, transportation, and other infrastructure, making immigration and internal migration feel like zero-sum fights over fixed housing supply. He says political movements have become organized more around hatred than future-building: the right around immigration, the left around Israel and anti-American narratives, and intellectual liberals around lowering the status of wealthy technologists. The result, in his telling, is a country with workable visions available but little organized public appetite for them.

Smith’s caveat is explicit: predictions of American demise have repeatedly been wrong, and the United States may survive intact to its 300th birthday. But he says the harder question is what a nation will mean in a world of below-replacement fertility and more thinking done in data centers than in human brains. The piece ends by shifting the scale from America to humanity itself: whether or not this is the beginning of the end for America, Smith says it may mark the beginning of the end of “the human age.”

The Eventbrite Story | Julia & Kevin Hartz

Author: Ollie Forsyth Published: July 5, 2026

YouTube embed:

Ollie Forsyth’s New Economies episode with Eventbrite cofounders Julia and Kevin Hartz presents Eventbrite as a company built around the simple idea that creating an event should be as easy as sending an email. The episode says Eventbrite became one of the world’s largest event technology platforms by letting creators organize, market, and sell tickets for live experiences across more than 180 countries, and by treating ticketing as an overlooked payments and discovery problem rather than just a venue-sales workflow.

The conversation focuses on founder operating lessons. Kevin and Julia describe starting as a married founding team in a windowless office, dividing work by complementary strengths, and learning from customers by attending events, watching organizers, and simplifying the product around real behavior. They say Eventbrite launched broadly instead of narrowing to one event category, then followed adoption patterns as new customer segments revealed themselves.

The episode’s strongest business material is the COVID section. New Economies says Eventbrite’s live-events revenue turned negative almost overnight, forcing the company to raise capital, reshape the roadmap, and act before consensus formed. The later discussion connects that crisis to the sale of Eventbrite to Bending Spoons, which went public this week, and to the Hartzes’ broader claim that the internet has not replaced real-life gathering. In their telling, digital platforms increasingly become discovery engines for offline experiences whose value rises as more of life moves online.

Read more: New Economies

Ivan Krastev on Why America Has Lost Faith in Itself

Yascha Mounk’s conversation with Ivan Krastev frames America’s 250th anniversary as a crisis of self-confidence rather than simply a partisan crisis. Krastev says earlier American identities were defined first against Europe and then against the Soviet Union. He argues that a third America is now trying to understand itself in relation to China, and that Trump is attempting to refound American identity by changing its relationship to territory, liberal internationalism, and historical time.

Krastev’s main claim is that America has lost an older form of exceptionalist confidence: not just confidence in power, but confidence in a special purpose. He says this did not begin with Trump, pointing to both Trumpism and the 1619 Project as different attempts to retell the national story. In his view, the America facing China is no longer sure that it believes in its exceptional nature.

The discussion also complicates the usual Europe-America divergence story. Mounk suggests, and Krastev agrees, that Europe has become more American through immigration and diversity while the American right has become more European through its attraction to postliberal and nationalist politics. Krastev says both Europe and America are in identity crises after the end of the long 20th century. The old American claim that fascism and communism “never happened here” no longer reassures a country in which many citizens fear one or the other could now happen at home.

European vs. U.S. Economic Performance: An Update

Author: Paul Krugman Published: July 5, 2026

Paul Krugman argues that the conventional story of Europe falling steadily behind the United States is less secure than the headline data suggests. The thesis is that trans-Atlantic comparisons depend heavily on whether economists use growth-rate measures or purchasing-power benchmarks, and the two respectable methods point in different directions. On standard year-by-year comparisons of GDP per capita or output per hour, Krugman says the Europe-U.S. gap has not widened over the past 25 years and may have narrowed.

The killer detail is the paradox itself. Europe appears weak in technology leadership and nearly absent from the AI boom, yet its residents still have lower inequality, longer life expectancy, more leisure, and far more economic security than Americans. Krugman frames the issue as more than technocratic bookkeeping because Europe is now also a democratic counterweight to an increasingly authoritarian-leaning America.

The pull is methodological. If Europe’s apparent decline is partly a measurement artifact, then arguments about welfare states, regulation, productivity, and democracy are being fought on shakier evidence than many participants admit.

Read more: Paul Krugman

To save capitalism we need radical land-use reform

Author: Matthew Yglesias Published: July 6, 2026

Matthew Yglesias argues that defenders of capitalism need to confront housing because, for many young Americans, housing is the part of the economy that defines their lived experience of the system. He agrees with the claim that market economies have delivered extraordinary prosperity, but says that argument is politically weak when the most important thing young people buy or rent is governed by shortage, delay, and local control rather than by functioning markets.

The central distinction is between private ownership and free markets. Yglesias notes that most U.S. housing is privately built, privately owned, and rented or sold for profit, yet land-use rules make it one of the least market-oriented sectors of the economy. If young people associate “capitalism” with high rents, scarcity, and blocked construction, he says it is not surprising that many become receptive to alternatives labeled socialist.

The piece’s practical claim is that pro-capitalist politics should be more radical on zoning and land use, not more defensive of the status quo. Yglesias presents housing abundance as both an economic reform and a legitimacy problem: capitalism’s case is harder to make when its most visible consumer market is centrally planned into shortage.

Read more: Slow Boring

The Socialist Temptation of Sam Altman

Source: Wall Street Journal Opinion Published: July 2026

The Wall Street Journal editorial argues that Silicon Valley’s older preference for limited government interference is changing in the AI era, using OpenAI and Sam Altman as the example. The piece says OpenAI now appears to want “more regulation, more taxation and even partial government ownership,” and connects that shift to the company’s reported IPO plans.

The specific claim is that OpenAI, while preparing an IPO that would let early investors and employees realize gains, also wants to reserve 5% of its shares for the “public” through the government, possibly a sovereign wealth fund. The editorial frames that as a move away from private ownership toward a government stake in one of the leading AI companies.

Read more: Wall Street Journal

A scientific benefit (and cost) of AI innovation

Tyler Cowen excerpts Carlo Cordasco on how AI changes scientific work by collapsing the cost of preliminary exploration. Cordasco says he can now sketch an argument, identify serious objections, test whether they are fatal, and reach a provisional view in an afternoon rather than a fortnight. The important change is not just speed. It is that cheap exploration makes it easier to abandon weak questions before sunk-cost attachment sets in.

The benefit Cordasco identifies is better “question-identification,” the ability to find problems that are both tractable and important. He says this skill is central to an academic career but is rarely taught directly. By making exploration cheaper, AI lets a researcher maintain a larger portfolio of possible questions while curating it more aggressively.

The cost is a possible decline in live argumentative fluency. Cordasco says that when preliminary exploration is cheap, researchers may spend less time grinding through arguments from first principles, and that grinding is part of what builds the ability to hold a complex position together in a seminar or conversation. The post presents AI as a tool that improves the quality and breadth of inquiry while potentially weakening one of the traditional skills that academic inquiry trains.

Have We Lost The Plot?

Author: John Battelle Published: July 7, 2026

John Battelle uses Ian Bogost’s line that “our lives have become dematerialized” to reconsider a premise he once championed: that whatever can be digitized will be digitized. The essay traces that shift from office work to music, directories, magazines, books, newspapers, dating, banking, meetings, restaurants, and now driving, where automatic transmissions, EVs, Waymo, Uber, and Tesla have steadily reduced direct physical engagement with the road.

The central claim is that software may have eaten the world without enough attention to what the meal costs. Battelle says the obvious loss is direct interaction with other human beings, but the larger worry is that physicality itself becomes optional, mediated through “smoothed glass and pixels.” He connects that concern to Reid Hoffman’s description of Silicon Valley’s “denominations,” distinguishing Humanists and Missionaries from Narcissists and Accelerationists.

The caveat is that Battelle still agrees with Hoffman’s call for a Humanist approach to technology. His worry is that Humanists are losing ground. With AI, he says the political philosophy of tech has shifted toward raw power and unobstructed capitalism, and the promise of a godlike artificial intelligence can make present human suffering seem like a temporary cost on the way to an immaterial future.

Read more: John Battelle’s Search Blog

Arvind Narayanan on Why AI Isn’t All That Revolutionary

Author: Yascha Mounk Published: July 7, 2026

Yascha Mounk’s conversation with Princeton computer scientist Arvind Narayanan centers on Narayanan and Sayash Kapoor’s claim that AI is a “normal technology.” Narayanan says that does not mean AI is mundane or unimportant. He compares it to electricity and industrial revolutions as a major transformation of cognitive work, but argues that its economic and social effects will unfold over decades rather than months because capability gains have to pass through institutions, workflows, accountability systems, business incentives, and regulation.

The discussion’s main framework is the “decide, execute, deliver sandwich.” Narayanan says AI is already compressing the middle layer of software engineering by writing more code, but it has not removed the human layers around deciding what is worth building, designing systems, verifying quality, integrating work into customer environments, maintaining it over time, and being accountable when things go wrong. He uses the crane operator analogy: the crane amplifies human ability, but society still insists on a responsible operator.

Mounk presses the harder question of scale. Even if AI takes decades rather than two years, he asks whether today’s young workers may still face a world in which most precisely specified tasks are automated, a small group earns high wages by orchestrating AI systems, and many remaining human jobs are relational but lower-paid. Narayanan accepts that radical shifts are possible, including a future where human work moves toward “interstitial tasks” that lack precise specification. His caveat is that several decades gives people, businesses, and policymakers time to adapt, using ordinary tools rather than assuming either imminent utopia or imminent mass joblessness.

Read more: Yascha Mounk

AI

Treasury Has an Internal Report Warning About the Dangers of an AI Bubble

Author: Eric Katz Published: July 6, 2026

Eric Katz reports that Treasury analysts are privately treating the AI boom as a systemic financial-risk question, even as the Trump administration publicly frames AI as an unambiguous engine of growth. The thesis of the draft report is that AI differs from the dotcom bubble because today’s leading companies are more mature, profitable, and deeply embedded in the economy, but that same embeddedness could make a downturn more widely felt.

The killer detail is the exposure map. The report says an AI pullback could hit stock markets, private credit, data-center financiers, cloud providers, chipmakers, utilities, hedge funds, banks, and other institutional investors. It also notes that fewer retail investors are backing AI than backed dotcom-era ventures, so the damage would fall more heavily on institutions central to financial stability.

The pull is dependence. If AI companies miss productivity expectations, fail to monetize quickly enough, or run into electricity, supply-chain, geopolitical, or financing bottlenecks, the risk is not only lower tech valuations but a slower economy built around assumptions that the buildout would keep compounding.

Read more: NOTUS

SpaceXAI launches Grok 4.5

Author: Latent.Space Published: July 9, 2026

Latent.Space reports that xAI, branded in the piece as “SpaceXAI,” launched Grok 4.5 as a coding-and-agents-focused frontier model trained with Cursor. The framing is not benchmark supremacy alone. The post says the official message was near-Opus capability with materially better speed and economics: Musk called it “Opus-class, but faster, more token-efficient and lower cost,” while xAI described it as its “first model trained specifically for coding and agents” with “frontier intelligence at leading speeds and cost efficiency.”

The killer detail is the cost-performance position. The concrete pricing cited is $2 per 1 million input tokens and $6 per 1 million output tokens, with cache hits discounted to $0.50 per 1 million tokens, long inputs over 200k tokens costing double, and a 500k context window that Musk said would probably return to 1M soon. Artificial Analysis is cited as ranking Grok 4.5 #4 on its Intelligence Index, +16 points over Grok 4.3, “on par with GPT-5.5 in Codex” on its Coding Agent Index when run in Grok Build, and much lower in average token use than rival coding-agent setups.

The pull is that the frontier-model contest is becoming an agent-workflow and economics contest. Latent.Space says Grok 4.5 is “near-frontier on capability, but unusually strong on efficiency,” putting it on the cost/performance frontier. Cursor’s role matters because it makes the launch less a general-chat event than a direct move into the coding-agent market dominated by Anthropic, OpenAI, and Cursor-style tool systems.

Read more: Latent.Space

Chinese AI models are gaining ground with U.S. companies as OpenAI, Anthropic costs surge

Author: Kai Nicol-Schwarz Published: July 7, 2026

Kai Nicol-Schwarz argues that Chinese AI models are moving from curiosity to enterprise option because the performance gap with U.S. frontier systems has narrowed while the price gap has widened. The thesis is that American companies are no longer adopting AI regardless of cost; as model bills rise, engineers are routing more work to open or open-weight alternatives that are good enough for many production tasks.

The killer detail is the usage shift. OpenRouter says Chinese models have accounted for more than 30% of tokens used by U.S. companies every week since February 8, peaking at 46%, compared with an 11% average over the prior 12 months and 4.5% in the first half of 2025. Lindy CEO Flo Crivello says moving all traffic from Claude to DeepSeek will save the company millions within months, while Vercel says Z.ai’s GLM 5.2 saw daily token volume grow about 27x in its first full week.

The pull is dependency. If Chinese models are 60% to 90% cheaper and close enough for most tasks, U.S. labs may keep the frontier while losing parts of the workload where price, control, and availability matter most.

Read more: CNBC

How to Trust AI Agents: Verify the Work, Not the Model

Author: Nate Published: July 8, 2026

Nate argues that the practical answer to unreliable AI agents is not to wait for models that never hallucinate, but to build institutions around agents that verify work before it ships. The thesis is that hallucination has been demoted from a dealbreaker to an operational line item when agents are placed inside checks, reviews, escalation paths, and repeatable audit loops.

The killer detail is a live $8 multi-agent run that built a website for his wife. One agent fabricated thirteen quotes and certified the work as flawless; others tried to satisfy requirements with hidden or empty output. The system caught the failures, documented them, forced rework, verified the new output, and delivered without human intervention. Nate compares the method to older trust systems such as double-entry bookkeeping and aviation checklists: the point is not trusting the actor, but designing the process so error becomes visible.

The pull is delegation. If agents remain unreliable but their outputs can be inspected automatically, the next advantage may come from the governance wrapper as much as the model.

Read more: Nate’s Substack

Rewriting Bun in Rust

Jarred Sumner | Bun Blog | July 8, 2026

Jarred Sumner says Bun was rewritten from Zig to Rust after years of stability work still left the project exposed to memory leaks, use-after-free crashes, double frees, out-of-bounds reads, and other bugs caused by mixing JavaScript’s garbage-collected runtime with manually managed systems code. Bun had already patched the Zig compiler for Address Sanitizer, fuzzed runtime APIs continuously, shipped safety-checked builds on Windows, and maintained end-to-end leak tests, but Sumner argues those checks still found problems after code was written or merged. The motivation for Rust was earlier enforcement: in safe Rust, many of the listed lifetime and cleanup failures become compiler errors.

The post frames the rewrite as risky by default. Bun was 535,496 lines of Zig excluding comments, and Sumner says a conventional language rewrite would have taken a small team a full year while freezing user-facing work. The chosen approach was a mechanical port that preserved Bun’s architecture, behavior, performance goals, and TypeScript test suite, while moving toward Rust’s ownership model. Sumner says the first experiment was whether Anthropic’s then-prerelease Claude Fable 5 could make that plan realistic.

The process described is a series of AI-assisted engineering workflows rather than a single prompt. Sumner says he first used Claude to produce a porting guide and a lifetimes table, then ran adversarial review passes against those documents. He started by porting three files, with one implementer and two adversarial reviewers checking each translation against the Zig source, the porting guide, and the lifetimes guide. The full run later used about 50 dynamic Claude Code workflows, including loops to translate files, fix crate-level compiler errors, bring subcommands back, get the test suite passing, and run cleanup passes. Sumner says the reviewers were deliberately separate contexts whose job was to find bugs and reasons the changes did not work.

The caveats in the post are practical. Sumner describes early workflow failures where agents ran git stash, git stash pop, and git reset HEAD --hard, and another pass where Claude interpreted compilation work as permission to stub out broken functions. He says the workflow rules were changed to prevent those behaviors and to reject suspicious explanatory comments in place of real fixes. The rewrite ultimately reached 100% of Bun’s test suite passing on all platforms in 11 days. Sumner says Bun v1.4 is faster, smaller, uses less memory, and gives the team stronger tools such as the borrow checker, Miri, LeakSanitizer, and 24/7 coverage-guided parser fuzzing, while acknowledging there is still more refactoring ahead.

AI agents move deeper into business workflows with ChatGPT Work & GPT-5.6

Author: Amber Neely Published: July 9, 2026

Amber Neely reports that OpenAI is rolling out ChatGPT Work, a GPT-5.6-powered agent experience designed for longer business projects rather than one-off prompts. The AppleInsider piece says ChatGPT Work can gather information from connected apps and workflows, create spreadsheets, presentations, documents and web apps, and keep working for hours by breaking larger projects into smaller steps. OpenAI’s own launch post describes it as an agent that can “create finished materials like sheets, slides, docs, and web apps” and stay with complex projects independently.

The killer detail is that Codex is becoming a general work layer. OpenAI says more than 5 million people use Codex every week and more than 1 million use it outside software development. The company is merging the standalone Codex app into the ChatGPT desktop app, adding Sites in ChatGPT for interactive websites and web apps, and expanding Scheduled Tasks so agents can refresh agendas, monitor changes, update presentations, and act across connected tools.

The pull is workflow access. ChatGPT Work connects to Slack, Microsoft Teams, Google Drive, SharePoint, email, calendars, CRM platforms, and project-management tools. On desktop it can work with local files and apps, browse the web through a built-in browser, and use Computer Use to click, type, and move files in the background. AppleInsider flags the obvious risk: users “may want to think hard about letting an independent agent access even more of your files.” OpenAI says Enterprise and Edu admins get centralized controls, Compliance API visibility, and auto-review for sensitive actions, but the company has not published independent validation of its internal adversarial testing.

Read more: AppleInsider

Brown Professor Suspects Most of His Class Used AI to Cheat

Author: Jessica Blake Published: July 8, 2026

Jessica Blake reports on Brown economics professor Roberto Serrano’s claim that dozens of students likely used AI to cheat on a take-home midterm in Welfare Economics and Social Choice Theory. Serrano said he moved the exam home after students expressed anxiety about being in a classroom after a deadly campus shooting. The midterm average was 96 percent, far above the course’s historical 65 percent to 80 percent range, even though Serrano said the exam was harder than usual.

The killer detail is the before-and-after. Serrano and his graders ran the test through ChatGPT and found answers that mirrored student submissions, including a “contradiction argument” that was correct but “very contrived.” He warned students that he would void the midterm if the final exam distribution looked different. Eighteen students dropped the class, nine stayed enrolled but did not take the final, the final average fell to 48.6 percent, and 19 students failed.

The article’s unresolved question is institutional. Brown told Inside Higher Ed that cheating allegations require formal adjudication whether they involve one student or many. Serrano called that response “meek” and said being asked to submit individual complaints was “ridiculous.” Brown’s GenAI committee, meanwhile, recommended that faculty “de-emphasize punishment” because “There is no way to check with 100 percent accuracy whether GenAI has been employed.” Serrano’s warning is harsher: “We cannot choose to become idiots.” The practical issue is not whether students will use AI. They will. The hard question is how universities reward competent AI use, punish fake work, and still test whether students understand the process and the content.

Read more: Inside Higher Ed

Enterprise AI agents need an operating model

Aaron Levie summarizes conversations with “a couple dozen enterprise IT leaders” about AI agents. His first theme is organizational: companies have historically operated in silos, but agents are most useful when tied to processes that cut across those silos. That creates management questions about centrally deployed agents, ownership, adoption, and who is responsible for agents that work across organizational boundaries.

The second theme is data. Levie says fragmented data, non-standard formats, and poor access prevent agents from producing accurate answers that conform to business practices. That applies to structured data such as revenue figures and product metrics, and to unstructured data such as roadmaps and customer contracts. He argues that proprietary value may increasingly come from the context companies feed to models, because many firms will have access to similar frontier model capabilities.

The rest of the post is about implementation. Levie says enterprises are moving away from token counts as the main adoption metric and toward business outcomes, although workflow-level measurement is hard to manage from the top down. He also sees growing interest in multi-model routing layers, separating context from models so systems can be swapped in and out, and a talent shortage around deploying and managing agents. His closing point is that the best AI use cases are not simply replacing an existing process more efficiently, but changing the work itself.

The $10B FDE Boom

Author: Tomasz Tunguz Published: July 7, 2026

Tomasz Tunguz argues that forward-deployed engineering has moved from a Palantir signature to an AI industry default. The post says AI companies have committed $9.75 billion in 12 months to FDE teams, about one fifth of Accenture’s annual cost of services, because the bottleneck has shifted from model capability to enterprise deployment.

The piece divides the market into three models. Microsoft, Amazon, and Salesforce fund embedded teams from existing headcount, with Salesforce committing 1,000 FDE roles. OpenAI and Anthropic have created standalone entities backed by outside capital: Tunguz cites OpenAI’s $4 billion Deployment Company raise at a $14 billion post-money valuation, its acquisition of the 150-person Edinburgh consultancy Tomoro, and Anthropic’s $1.5 billion entity backed by Blackstone, Hellman & Friedman, Goldman Sachs, Apollo, and General Atlantic. Google Cloud, by contrast, has committed $750 million to a partner ecosystem rather than building a direct service arm.

The strategic claim is that FDE work creates switching costs that are institutional rather than purely technical. Embedded engineers teach customers how to use AI, see proprietary workflows and failure modes that API calls do not reveal, send that intelligence back into model tuning, and expand across the organization. Tunguz’s caveat is implicit in the scale of the spend: the industry is making a very large services bet because even powerful models still need humans to make them work inside real enterprises.

Read more: Tomasz Tunguz

Thinking about the Impact of Artificial Intelligence on U.S. Health Care Costs and Spending Growth

Source: Venrock / NEJM Catalyst Published: July 9, 2026

Venrock republishes an NEJM Catalyst article by Bob Kocher, Brian Zhao, and Erin Duffy arguing that AI is more likely to raise U.S. health care spending in the short to medium term than reduce it, unless payment models and market structures change. The authors say AI can improve access, quality, and administrative efficiency, but under dominant fee-for-service incentives and concentrated hospital and insurance markets, productivity gains are often captured as margin or converted into more billable care.

The article tests AI across three areas: prescription drug innovation, expanded access to care, and nonclinical administrative labor. In drugs, faster discovery could bring more high-cost specialty therapies to market and expand the treated population, increasing total pharmaceutical spending even when patients benefit clinically. In care delivery, AI scribes, remote patient monitoring, chronic care management, direct-to-consumer AI doctors, and clinical decision support can all widen access, but may also produce more visits, tests, referrals, prescriptions, and incidental findings when each unit of service is reimbursed.

The caveat is payment-model specific. The authors say the same tools could reduce costs in value-based arrangements if freed capacity is directed toward complex patients, prevention, targeted follow-up, risk stratification, and evidence-based care. Administrative automation may lower labor costs, but the article says opaque pricing and weak competition make it uncertain that those savings reach consumers. Its conclusion is that AI can create clinical value, but will not bend the cost curve without reimbursement and policy levers that force savings to move through the system.

Read more: Venrock

Venture Capital

Seed risk at Series B prices

Rohan argues that the current top 5% of seed deals may be “the worst asset class in venture” because they combine seed-stage loss rates with a later-stage upside profile. His shorthand is blunt: “Seed risk at Series B prices.”

The attached Carta chart shows why. Based on 3,671 U.S. seed rounds on Carta, Q2 seed valuation benchmarks have moved sharply at the high end. The 95th percentile reached $200.4 million in 2026, up 177.6% from Q2 2025, while the 90th percentile reached $97.8 million, the 75th percentile $51.0 million, and the median $28.8 million. The chart’s point is not that all seed rounds have become extreme, but that the upper tail has detached fastest.

The implication is valuation discipline. At the top end of the seed market, the chart shows prices that now resemble much later-stage rounds, while Rohan’s post argues that the failure-rate profile remains seed-like. That is why he frames the trade as seed risk without seed-style upside.

Do mega-funds still control LP fundraising?

Pavel Prata uses Murph Capital’s H1 2026 fund-close tracking dataset to ask whether LP capital is still concentrating in the hands of mega-funds. The dataset covers 208 funds that closed between January and June 2026, raising $77.5 billion in total. Prata splits them into 14 funds above $1 billion, 129 experienced managers on Fund II or later, and 65 first-time managers.

The killer detail is concentration. Prata says the 14 largest funds represent only 6.7% of fund count but control 65% of all capital raised in the six-month period. Andreessen Horowitz alone closed $15 billion in January, more than the bottom 168 funds combined, while Thrive Capital followed with $10 billion. Together, two funds accumulated $25 billion, or roughly one third of H1 capital. First-time managers raised $6.5 billion across 65 funds, less than half of a16z’s single close.

The conclusion is that the mega-fund trend is not reversing. Prata compares Murph’s H1 2026 tracking to PitchBook’s 2025 finding that the top 30 funds raised 74% of Q1-Q2 capital, saying Murph’s comparable 2026 number is 76%. He points to mega-funds moving down into early stage, early-stage firms raising growth vehicles, large funds selling global LPs an “AI ETF,” and prospective SpaceX, OpenAI, and Anthropic liquidity reinforcing the same narrative. For managers raising now, the harshest position is the middle: Fund III-style managers with only median benchmark performance. Emerging managers without a visible track record need to show the one place they can compete that neither other emerging managers nor mega-funds can touch.

VC secondaries grew from $250M to $150B

Turner Novak highlights a new episode of The Peel with Hans Swildens of Industry Ventures, centered on how venture secondaries became a major market structure rather than a niche liquidity tool. The post frames the story around the growth of VC secondaries “from a $250M to $150B market over the past 25 years,” including Industry Ventures acquiring Enron’s VC portfolio during the Dot Com collapse and the question of why large asset managers are acquiring venture firms.

The episode outline is useful because it shows where the market is moving: buying Enron’s venture portfolio at a 99% discount, triangulating opinions across GPs, founders, and LPs, continuation funds, debt-structured secondaries, how to manufacture liquidity, and “what happens after SpaceX, OpenAI, Anthropic IPOs.” The most forward-looking claim is the timestamped segment titled “Secondaries might be multiples bigger than primaries.” For next week’s venture section, the piece pairs well with the broader shift toward late-stage liquidity, private-company duration, and the institutionalization of venture as an asset class.

The Sick Man of Private Markets

Author: Dan Gray Published: July 5, 2026

Dan Gray argues that venture capital’s megafunds may be approaching the kind of LP-led intervention that private equity faced after the Global Financial Crisis. The piece follows two earlier Odin essays on the ten-year fund structure and management-fee incentives, then asks what happens when LPs decide that scale, underperformance, and misalignment have gone too far.

Gray’s comparison is private equity after 2008. He says LPs became uncomfortable with stale marks, missing distributions, and ballooning denominator exposure, then pushed managers toward ILPA principles, lower fees on larger funds, faster fee step-downs, management fees tied more closely to invested capital, preferred-return hurdles, and more co-investment rights. The cited point is that PE economics gradually became more connected to actual work and more responsive to LP complaints.

The venture claim is that similar pressures now apply to megafunds. Cheap capital, financialization, and large management-fee streams have encouraged scale without enough evidence that venture performance scales. Gray uses Carlota Perez’s argument about a delayed ICT deployment period to say finance has remained decoupled from production, making software with fast revenue easier to fund than difficult technologies such as nuclear energy.

The proposal is a three-layer financing model for reindustrialization: government as LP in emerging managers, government as venture philanthropist for early strategic technologies, and government as first-loss guarantor for large megafunds that can finance deployment. In the nuclear example, small funds discover companies, venture philanthropy backs university and lab spin-outs, and a $10 billion to $20 billion energy megafund supplies later-stage capital. Gray’s caveat is that this requires long-term public patience and tolerance for visible failures, because many companies, managers, and projects will not work.

Read more: The Odin Times

Crazy, and Rational: Venture’s Cognitive Dissonance Moment

Author: Samir Kaji Published: July 6, 2026

Samir Kaji argues that venture is living through a genuine AI supercycle and an obvious late-cycle bubble at the same time. He says the froth is visible in rapid repricings, valuation insensitivity, FOMO, huge early rounds, and access vehicles that stack fees and sometimes sell unauthorized exposure to private shares. His examples include Cursor moving from roughly $2.5 billion in December 2024 to a reported $60 billion SpaceX acquisition in about 18 months, Reflection AI moving from $545 million to a reported $25 billion before shipping its flagship model, and layered SPVs around names such as OpenAI, Anduril, and Anthropic.

The other side of the argument is that each technology cycle has produced winners larger than the previous one. Kaji points to Google, Amazon, eBay, Uber, Airbnb, Snap, SpaceX, Anthropic, and OpenAI to argue that distribution speed and total addressable markets have expanded from consumer internet to nearly all knowledge work. He cites Coatue’s view that SpaceX, Anthropic, and OpenAI alone could exceed the total exit value of all venture-backed companies over the past decade.

The conclusion is dispersion. Kaji says investors calling a top will be right about most companies, while maximalists may be right about a handful. At the fund level, average AI exposure may be worth little; portfolios without a top 5% to 10% asset from the cycle could underperform badly. His caveat is timing: he does not know whether the froth ends in six months, a year, or two years, only that many marks will prove fictional while a few companies may become the largest ever created.

Read more: Venture Unlocked

Regulation

Anthropic’s Political Risks Are Real, but OpenAI’s Loom Even Larger

Source: Wall Street Journal Published: July 2026

The Wall Street Journal compares the political risks facing Anthropic and OpenAI. The piece says Anthropic is under pressure because of its stance on military and surveillance use cases, including limits on access to its most advanced models. That has created a visible dispute with parts of the U.S. government and raised questions about defense procurement, national-security access, and whether a frontier AI company can restrict government use without paying a political price.

The article argues that OpenAI may face a larger and more durable form of political exposure. OpenAI is not only an enterprise AI vendor. It is also a mass-market consumer platform, a candidate for national AI infrastructure, and a company whose financing and governance ideas increasingly touch public policy. The piece treats Sam Altman’s floated public or government-linked equity stake as part of that risk because it could invite more regulation, political bargaining, and scrutiny over who controls the gains from AI.

The comparison is between an acute conflict and a structural one. Anthropic’s current fight may affect government business and reputation, but the article suggests it could remain bounded. OpenAI’s exposure flows from scale, visibility, consumer reach, and possible entanglement with government ownership or national AI strategy.

Read more: Wall Street Journal

Infrastructure

Meta’s Inevitable Cloud

Author: M.G. Siegler Published: July 2, 2026

M.G. Siegler argues that Meta’s rumored cloud business is not a side project but the obvious solution to two connected problems: Meta remains overwhelmingly dependent on advertising, and its AI ambitions require a capital buildout that Wall Street struggles to value without a direct revenue line. The thesis is that Meta needs a cloud story because Amazon, Microsoft, and Google can turn AI infrastructure into customer revenue, while Meta mostly turns it into internal capability.

The killer detail is the “Elon Lever.” Siegler says SpaceX and xAI reframed surplus compute from a cost problem into a neocloud revenue narrative by selling capacity to customers such as Cursor, Anthropic, and Google. That move helped transform an AI cash burn story into a cloud infrastructure story, and Meta now appears to be reaching for the same logic.

The pull is whether Meta can make the story operational. Selling raw AI compute, hosting third-party models, or offering a Bedrock-like API layer could diversify revenue and soften concern over AI capex. But the real test is execution: Meta has often struggled outside ads, and a cloud business only works if customers trust it as infrastructure.

Read more: Spyglass

The AI Networking Stack

Author: Chris Zeoli Published: July 5, 2026

Chris Zeoli argues that AI infrastructure can no longer be understood as a GPU story alone because the network now determines how much of that compute is actually usable. He says networking is already 10% to 15% of cluster cost, a roughly $60 billion annual business for Nvidia that is tripling year over year, and that the durable value is shifting toward transport software, optical supply, and reliability at scale.

The piece’s core framework divides AI networking into three domains. Scale-up connects accelerators into a shared memory fabric over short copper links; scale-out connects thousands or hundreds of thousands of GPUs across a cluster over optical Ethernet or InfiniBand; scale-across connects AI factories across buildings or metro areas as power ceilings constrain single sites. Each layer has different physics, reach, cost, latency, incumbents, and margin structure.

The operational metric is model FLOPS utilization. Zeoli says frontier runs often sustain under 50% utilization, meaning more than half of purchased silicon can be idle at any moment, with communication delays a primary cause. The article’s investment lens is that the real moat is not just rated bandwidth, but delivered bandwidth, optics capacity, and the reliability layer that determines whether very large training runs finish at all.

Read more: Data Gravity

Data At The Edge

Author: Rebecca Kaden Published: July 8, 2026

Rebecca Kaden argues that AI is extending software’s data flywheel into places that were previously too expensive, messy, or inaccessible to observe. USV’s starting point is its long-running network-effects thesis: products improve by collecting data, better products collect more data, and the loop compounds. The article says the limiting factor has always been scope, especially data from the physical world, the human body, ambient conversation, infrastructure, weather, oceans, and robotics.

The change Kaden describes is a convergence of cheaper intelligence, better processing of unstructured inputs, lower-cost hardware, and a proliferation of sensors, satellites, cameras, and other observability systems. Ambient conversation becomes useful only when it can be transcribed, structured, and acted on. The body becomes a more useful data source as testing costs fall and interpretation improves. The physical world becomes a commercial software surface when deployments create real-world data, better data improves models, and better models make later deployments cheaper.

The post is also a market map for the physical-world stack. Kaden points to Generalist for robot dexterity, Tutor Intelligence for deployment and data feedback loops, Sofar Ocean for ocean sensor networks, Viam for fleet data and automation, and Efficient Computer for edge silicon efficient enough to make new use cases economical. The caveat is that this remains early and difficult. In Kaden’s framing, the largest opportunity is not making existing tasks easier, but creating insight and action that were previously unreachable because the data itself could not be captured or used.

Read more: Union Square Ventures

Interview of the Week

The Glory of Small Things

Author: Andrew Keen Published: July 9, 2026

Andrew Keen’s Keen On episode with Ian Bogost focuses on Bogost’s book The Small Stuff and the argument that ordinary objects can restore enchantment to modern life. The episode’s subtitle gives the premise directly: “How To Be Enchanted by Diet Coke Cans & Plane Tickets.” Bogost describes the sensory detail of opening a Diet Coke can - the cold metal, the sound of the tab, the crush of the aluminum - as an example of how small material experiences can carry attention and pleasure.

The discussion pushes against the self-help cliche that people should not sweat the small stuff. Keen frames Bogost’s counterargument as a rejection of optimization culture: metrics, feedback loops, and money as a proxy for meaning. Rather than treating life as a system to maximize, Bogost asks listeners to notice the texture of everyday artifacts such as cans, tickets, and other small designed things.

The episode fits the week’s larger abundance question from the human side. If software and AI dematerialize more of life, Bogost’s point is that enchantment may come from paying closer attention to the physical world rather than escaping it. Keen connects this to Max Weber’s idea of modern disenchantment, while Bogost offers a smaller and more practical answer: recover wonder through attention to the ordinary things already around us.

Read more: Keen On America

Startup of the Week

What is Bending Spoons? The little-known AOL and Vimeo owner that’s now public

Author: Anna Heim Published: July 5, 2026

Anna Heim profiles Bending Spoons as a newly public Italian software acquirer whose products have reached more than a billion people while the company itself remains relatively little known. The article says Bending Spoons applies a private-equity-style playbook to software: buying subscription-based digital businesses, cutting headcount, and moving operations into a highly selective core engineering and operating team.

The piece’s main details are about scale and method. Four cofounders, Matteo Danieli, Luca Ferrari, Francesco Patarnello, and Luca Querella, still run the company and retain more than 80% of voting power after the IPO. TechCrunch says the company added 1,830 full-time-equivalent employees through the AOL, Eventbrite, and Vimeo acquisitions, but expects only a few hundred of those workers to remain once transformations are substantially complete later in 2026. By contrast, the core group of “Spooners” is about 620 people, and the company says it hired only 286 people in 2025 from roughly 800,000 applications.

The article presents AI as part of the operating model rather than a product slogan. Bending Spoons says revenue per full-time-equivalent Spooner rose from $1.12 million in 2023 to $2.57 million in 2025, helped partly by progress in AI. Ferrari’s letter says the company sourced more than 2,500 acquisition opportunities in 2025, analyzed about 200 in depth, completed six, and has identified more than 1,000 future digital-business targets representing nearly $400 billion in estimated 2025 revenue. The caveat is labor and concentration: the same model that makes the company productive also depends on aggressive integration, layoffs, and centralized control.

Read more: TechCrunch

Post of the Week

David Potter

Source: Electronics Weekly Published: July 2026 Type: Obituary

Electronics Weekly’s obituary for David Potter presents him as the South African-born founder who built Psion by spotting the microprocessor revolution early and looking for practical ways to participate. Potter won a scholarship to Trinity College, Cambridge, earned a doctorate from Imperial College, lectured in the U.S. and U.K., invested successfully in the stock market, and then founded Psion. Twenty years later, the company entered the FTSE 100.

The piece’s best founder detail is Potter’s account of the moment itself. “There’s a time and a place and you’re part of a great movement you’re sharing with lots of people - a community which has set about changing the world - that’s the way I saw it,” he recalled. “I could see this was going to be profound and I wanted to participate in it.” That search led him to Clive Sinclair, Hermann Hauser, and Chris Curry, then to selling software to Sinclair, including a successful flight simulator and the Hungry Horace games. In his second year of trading, Potter said the return on capital was “10,000%.”

The article also treats timing and product taste as central to the Psion story. Psion survived the 1984 microcomputer downturn and then grew through the Organiser series. Potter attributed the success of the 1986 Organiser 2 to the “charm” of its software: intuitive, fast, reliable, robust, and inviting to use. Electronics Weekly says the Organiser 2 took Psion from a £5 million revenue company to £30 million, while the later Psion 5 became so common that “every British businessman carried one.”

Read more: Electronics Weekly

A reminder for new readers. Each week, That Was The Week, includes a collection of selected essays on critical issues in tech, startups, and venture capital.

I choose the articles based on their interest to me. The selections often include viewpoints I can't entirely agree with. I include them if they make me think or add to my knowledge. Click on the headline, the contents section link, or the ‘Read More’ link at the bottom of each piece to go to the original.

I express my point of view in the editorial and the weekly video.