$4 Trillion of Unicorns

By Keith Teare • Issue #298 • View online

Content

Editorial

Crunchbase News tells us that the company has updated its Unicorn Board and that:

There are 59 so-called decacorns—companies valued at $10 billion or more—within the group. Just a year ago, there were only around half that count, at 31 decacorns.

Three of these decacorns are valued above $100 billion and stand as the most valuable private companies in the world: Shanghai-based TikTok owner ByteDance, valued at $180 billion; payments platform Hangzhou-based Ant Group, at $150 billion; and Hawthorne, California-based space travel company SpaceX, at $100 billion.

The Crunchbase board is a great asset. But it seems that we should soon see more than a single board. The unicorn board has 591 2021 vintage unicorns (and that does not include the 240 or so companies that exited above $1 billion in 2021 but were not unicorns prior to their exit). Over 800 $1 billion values in 2021 alone. A unicorn board is useful but there is a need now for a decacorn board, a centicorn board and who knows how soon we will see private company values well above $100 billion?

The pace of unicorn production is staggering, and accelerating, to the point that it is becoming ordinary to be a unicorn. And that is not explained by any “bubble”. It is mainly the result of the market opportunities available and the speed at which companies are making progress in growing their businesses. This is all fueled by the abundance of capital available to energize the companies pursuing those opportunities.

But that momentum provides a canvas on which the venture capital industry is evolving. The latest news, highlighted this week, is that Tiger Global and D1 - two of the most prolific allocators of capital, are planning to shift strategy. Berber Jin of The Information covers that news. Tomasz Tunguz writes about the consequences of that change. He posits that 2022 could see a counter-trend to the reduction in public market values. He explains why series A and B round values might go up in light of the new capital Tiger, D1 and others may bring to the earlier stage investment table.

This is further evidence of the trend we have covered here - that of large allocators coming earlier and earlier into the venture ecosystem. We have explained in the past that there are three asset classes within venture. The seed, venture and growth stages. Normally the pre-seed, seed and Series A stages are thought of as early stage, Series B, C and D as Venture and Series E and later as growth.

Those assumptions may be challenged as larger allocators are prepared to invest at the still risky A round stage. And seed stage investors will be challenged to do their pro-rata - which today kicks in at the B round, but may now focus more on the A round.

For those not versed in the specifics of venture capital these may seem like unimportant points, but they will shape the entire venture ecosystem over the next few years. And large amounts of money will be impacted.

At SignalRank we keep a live view of the ecosystem. Looking at the 2021 unicorns is interesting.

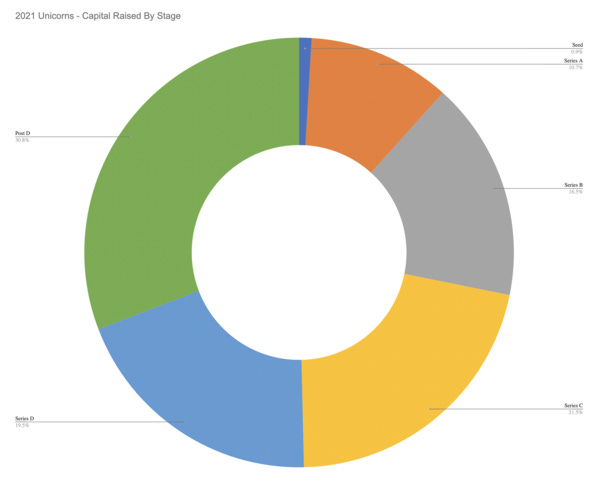

They collectively raised the following amounts round by round:

Prior to the A Round: $1.7 billion

At the A Round: $19.5 billion

At the B Round: $30 billion

At the C Round: $39 billion

At the D Round: $35.5 billion

Post D Round: $56 billion

88.35% of all capital raised came after the A round. If large allocators invest earlier the equation will change. This has implications for seed investors and also for early stage venture investors. It likely means that growth investors will also move from the E, F and later rounds to the B, C and D rounds, increasing the dilution experienced by seed investors at those stages. The trend to value growth happening when a company is pre-IPO will accelerate. Thanks to Gené Teare and Crunchbase for their work.

The content below is for subscribers only

Please Subscribe Now